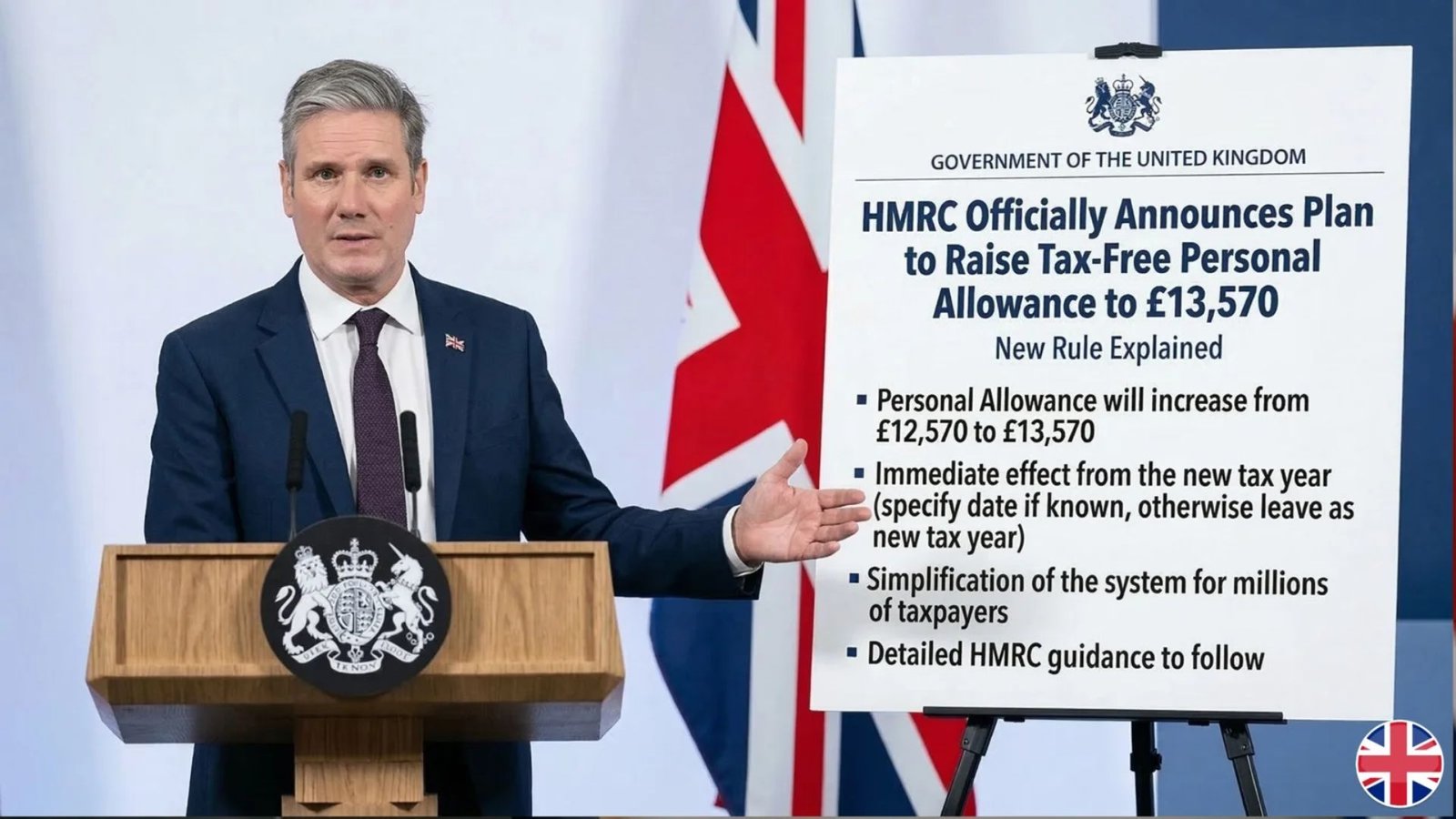

The UK tax system may soon see an important change as discussions continue about raising the tax-free Personal Allowance to £13,570. If implemented, the update would allow millions of workers to earn more income before paying Income Tax.

The Personal Allowance is a key element of the UK tax structure because it determines how much of an individual’s earnings are tax-free. Any increase in this threshold can directly affect take-home pay for employees, pensioners, and self-employed individuals.

Below is a clear explanation of how the potential change works and who could benefit from it.

What Is the Personal Allowance?

The Personal Allowance is the amount of income a person can earn each tax year without paying Income Tax.

Currently, most UK taxpayers can earn £12,570 per year tax-free before the standard 20% basic Income Tax rate applies.

If the allowance increases to £13,570, individuals would be able to earn an additional £1,000 tax-free before Income Tax is charged.

Even a relatively small increase like this can lower the overall tax bill for millions of people.

Why the £13,570 Threshold Matters

Raising the Personal Allowance to £13,570 means the first portion of a person’s income would remain tax-free.

For someone paying the basic 20% tax rate, a £1,000 increase in the allowance could reduce their yearly tax bill by around £200.

While this may appear modest, it can help households dealing with rising living costs by slightly increasing monthly take-home pay.

Who Would Benefit the Most?

An increase in the Personal Allowance would mainly help people whose income is above the current threshold but still within the basic tax band.

Those who may benefit include:

- Full-time employees

- Self-employed individuals

- Pensioners receiving taxable pension income

- Part-time workers earning near the tax threshold

People whose income is already below the Personal Allowance would not see a direct change, as they already pay no Income Tax.

How the Change Would Work in Practice

If the allowance rises to £13,570, it would automatically reduce the portion of income that is taxable.

Example:

If someone earns £25,000 per year, the calculation would work like this:

- £13,570 – tax-free allowance

- £11,430 – taxable income

Only the taxable portion would be charged Income Tax.

Employees typically receive the benefit automatically through the PAYE payroll system, while self-employed individuals apply it when filing their Self Assessment tax return.

Important Rules for Higher Earners

The Personal Allowance is not available in full for everyone.

For individuals earning more than £100,000 per year, the allowance gradually decreases. The reduction occurs at a rate of £1 lost for every £2 earned above £100,000, which can eventually remove the allowance entirely.

Because of this rule, higher-income earners may receive little or no benefit from a potential increase.

Difference Between Income Tax and National Insurance

It is important to understand that the Personal Allowance applies only to Income Tax.

National Insurance contributions follow separate rules and thresholds. Even if the Personal Allowance rises, National Insurance payments may remain unchanged.

This is why the change may slightly increase take-home pay but will not remove other deductions.

When the New Allowance Could Start

If the proposal is approved, the updated Personal Allowance would likely begin at the start of a new UK tax year.

The UK tax year starts on 6 April, so any confirmed increase would normally apply from that date and continue through the entire tax year.

Payroll systems and tax codes would be updated automatically to reflect the new threshold.

Why the Personal Allowance Has Been Frozen

In recent years, the Personal Allowance has remained unchanged at £12,570 despite rising wages and inflation.

This situation is often referred to as “fiscal drag,” where more income becomes taxable over time even if tax rates do not change.

Increasing the allowance could help offset some of that effect.

What This Means for Workers and Pensioners

If the threshold rises, many taxpayers would see a small increase in their take-home pay spread across the year.

For pensioners with taxable pension income, the higher allowance could also reduce the portion of their pension that is taxed.

However, the exact benefit will depend on individual income levels.

Key Points to Remember

- The Personal Allowance determines how much income is tax-free.

- The current threshold is £12,570 for most UK taxpayers.

- A proposed increase to £13,570 would allow people to earn £1,000 more tax-free.

- Basic-rate taxpayers could save around £200 per year.

- Higher earners above £100,000 may see limited benefits.

FAQs

Is the £13,570 Personal Allowance confirmed?

At present, it is discussed as a proposal and would require official approval through government legislation before becoming permanent.

When would the new allowance start?

If approved, the change would most likely begin at the start of a new tax year on 6 April.

Will National Insurance also be reduced?

No. The Personal Allowance affects Income Tax only, while National Insurance uses separate thresholds.

Do employees need to apply for the new allowance?

No. Most employees will receive the benefit automatically through their PAYE tax code.

Will pensioners benefit from the increase?

Yes, pensioners whose total income exceeds the allowance may pay slightly less Income Tax if the threshold increases.